Introduction

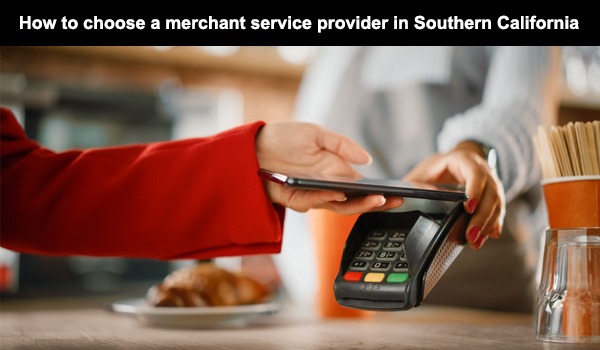

Picture this: A sunny day in California, and your retail store is bustling with customers. The one thing as common as the sunshine? Credit cards swiping at your registers. In today's retail environment, accepting credit cards isn't just an option; it's a necessity. But, with great convenience comes the sometimes perplexing world of processing fees. We're here to make that world a little less daunting.

Deciphering the Fundamentals of Credit Card Processing Fees

Alright, let's break down these not-so-fun fees together.

Transaction Fees

Every time a customer swipes, dips, or taps their card at your store, you're paying a transaction fee. It's a tiny percentage of the sale, plus a few cents on top. For us California retailers, these fees average around 2% to 3% of the transaction amount. Compared to some other states, we're right there in the middle. Not the cheapest, but not the priciest.

Interchange Fees

Imagine interchange fees as the price of admission to the credit card club. These fees go to the bank that issued the customer's card, and they fluctuate based on a bunch of factors like card type and transaction size. In California, there's no escaping these fees, but a good understanding can help you predict them better and possibly even lower them by optimizing your payment acceptance methods.

Tip: Using more secure transaction methods like EMV chips can sometimes help you snag lower interchange fees.

Assessment Fees

These are the fees charged by the card networks (Visa, MasterCard, etc.), and they're usually a fixed percentage of your monthly sales volume through their cards. Like a toll road fee for your transactions to travel on their network highways. Each network has its own set of rates, but the good news is, that with the right negotiation and provider, these costs can be manageable.

Types of Credit Card Processing Pricing Models

Different strokes for different folks, right? Here's a lowdown on the pricing models you might encounter.

Tiered Pricing

This model might remind you of a traffic light: transactions are categorized into tiers (green, yellow, red), each with its own rate. It sounds straightforward, but the kicker is figuring out which transactions fall into which tier. For us in California, facing average-tiered pricing fees means doing your homework and understanding where your most common transactions are likely to come under.

Interchange-Plus Pricing

Think of this as your retail operation's best buddy. It's transparent, showing exactly what the interchange fee is plus a fixed markup from your processor. It's a favorite among many for its openness, and it generally offers California retailers a fair deal. Expect interchange-plus rates to hover around the average transaction cost but with a clearer breakdown.

Subscription or Membership-Based Pricing

This model is like your Netflix subscription but for processing payments. You pay a monthly fee for the privilege of processing transactions, plus a tiny transaction fee. It's newer but gaining traction for its predictability and can make sense if you're running a high-volume business.

Additional Fees and Hidden Costs

Here's where it gets a tad annoying. Keep an eye out for these.

Monthly and Annual Fees

Many processors tack on monthly or annual fees for account maintenance or software access. It varies wildly, so comparing providers is key. And don't be shy about bargaining — sometimes, these fees can be reduced or waived.

PCI Compliance and Non-Compliance Fees

PCI compliance is all about keeping your customer's payment info safe. There's usually a fee involved in maintaining these security measures, but it's a small price to pay for your customer's trust. Slip up, though, and non-compliance fees can bite. Better to be safe than sorry!

Chargeback Fees

The dreaded chargeback — when customers dispute a charge, and it comes back to haunt you. Not only is it a hassle, but it also comes with fees. Prevention is your best bet here, with clear return policies and prompt customer service.

Choosing the Right Credit Card Processor for Your Retail Business

Here's where we bring it all home. When picking a processor, think beyond just fees. Consider how reliable their service is, how well they'll integrate with your current systems, and the flexibility of their contract terms. Your processor should be a partner, not just another vendor.

Understanding Your Statement

Once you're all set up, don't let your monthly statements become just another paper on the pile. Review them regularly to understand the fees you're being charged, and don't hesitate to ask your processor if something looks off. It's also a great tool for negotiations down the line.

Remember: The world of credit card processing fees might seem daunting, but knowledge is power. The more you know, the better you can navigate this complex arena, turning potential headaches into opportunities for savings.

Navigating Payment Processing Costs

Advantages of Understanding and Managing Fees

Getting a handle on these fees can lead to:

- Improved Profit Margins: Every penny saved on fees is a penny added to profits.

- Better Pricing Strategies: Understanding fees can help you price products more effectively.

- Enhanced Customer Experience: Offering various payment options without exorbitant fees can boost customer satisfaction.

Strategies for Managing and Reducing Fees

Here are a few tactics:

- Negotiating with Providers: Sometimes, rates are not set in stone.

- Assessing Your Needs: Don’t pay for services you don’t use.

- Comparison Shopping: Look around before settling on an MSP.

- Optimizing Payment Methods: Encouraging cheaper payment methods can save you money.

Technology and Tools

Leveraging technology can also play a big part in managing costs:

- Integrated Point of Sale (POS) Systems: Can help streamline transactions and reduce errors.

- Advanced Payment Gateways: For optimizing online sales and possibly getting better rates.

- Utilizing Data Analytics: Understanding your sales data can help you make informed decisions about payment processing.

Legal and Regulatory Considerations in California

State Regulations on Credit Card Fees

California has specific regulations about surcharging customers and how much can be passed on to them for credit card transactions.

Consumer Protection Laws

Keeping abreast of these can not only save you from legal headaches but also enhance your store’s reputation.

Conclusion

And there you have it, a journey through the maze of credit card processing fees. Remember, these fees can be a significant expense for California retailers, but they're also an area rife with opportunities for savings. Stay informed, ask questions, and always be on the lookout for a better deal. Your bottom line will thank you!

Here's to making more informed decisions and keeping more of our hard-earned money in our pockets!