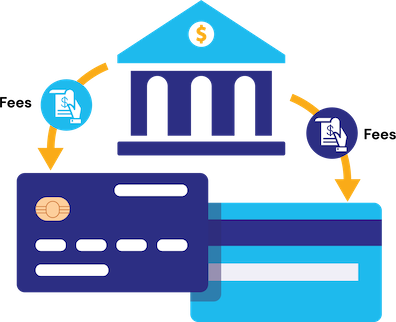

We help merchants to reduce or eliminate their processing fees as much as we can, in addition to efficiently managing the interchange fees.

Overview:

Q PaymentZ firmly believes in always giving the best to its customers. Bringing to you the new and unique ‘Efficient Interchange(EI)’ Program. Not only do we strive to bring down your processing fees, but we also aim to bring down the interchange cost of transactions that you process.

Visa & MasterCard require additional information beyond the total sale amount to qualify the Commercial Card transaction for a lower interchange rate. This information includes the sales tax amount, which, if provided, reduces the merchant’s interchange cost. We will compute and submit the required sales tax to the Card networks for applicable Commercial Card transactions. When this additional data is provided, it allows these transactions to qualify for a lower interchange rate.

Benefits:

Merchants receive the best possible interchange category and rate per purchase for the card type accepted by submitting line-item information to Visa and Mastercard.

Our Efficient Interchange(EI) brings potential savings, sometimes even to a max of 90 basis points (0.90%) from Interchange.

Features:

Transactions are identified by card Bank Information Number (BIN) range, ensuring the appropriate information is defaulted and passed to card issuers.

Qualification is based on transactions that are identified by card type.